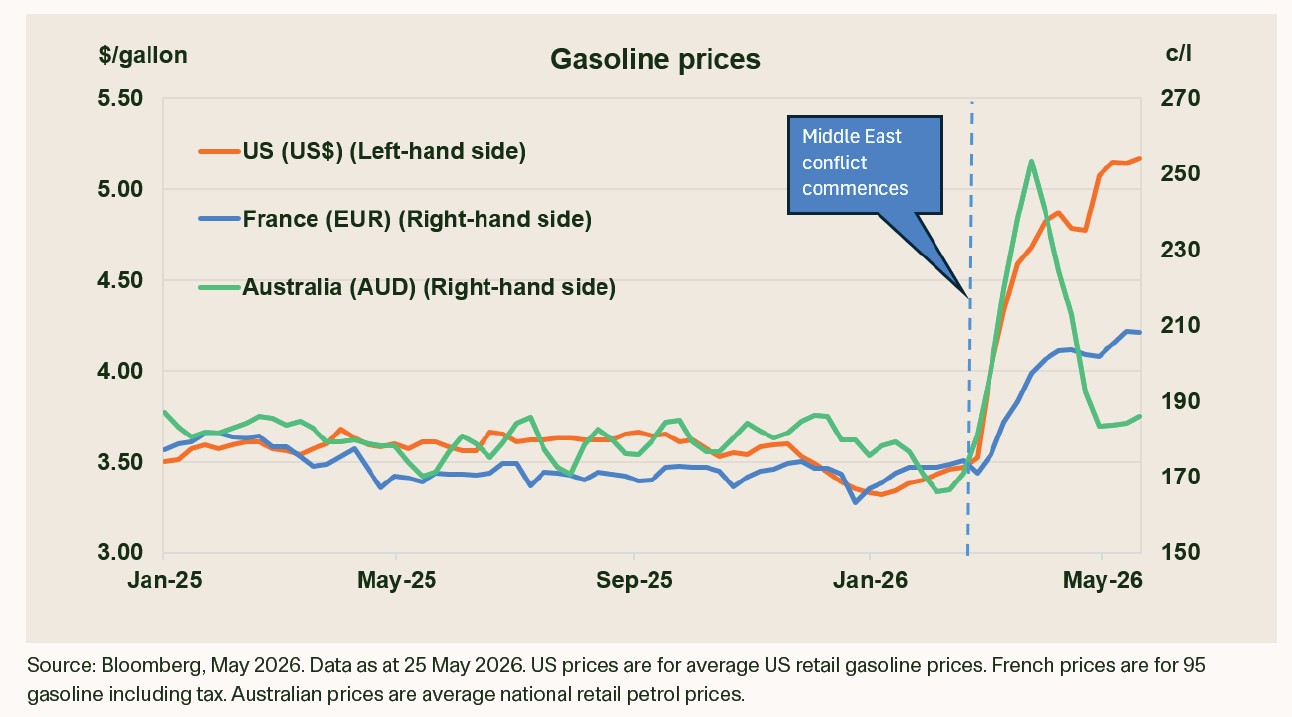

With the Strait of Hormuz remaining largely shut, oil prices remain elevated. In consequence, petrol prices to consumers have jumped in recent months and are persisting and high levels. Average US gasoline prices are up 47% since 27 February 2026, and in France, retail petrol prices have risen more than 20% over this period.

This matters for infrastructure as higher gasoline pricing can eat into household budgets and can dampen demand, particularly for toll roads. Even in wealthy countries, where gasoline is a small share of average consumer outlays, households can have outsized sensitivity to higher prices at the pump.

This pattern in activity is showing up in traffic data across some major toll road networks. For example, Vinci reported a 5% y/y decline in volumes on its autoroutes in April, with car traffic the key driver (down 6.0%y/y). The company attributed the weak performance to the sharp rise in fuel prices at the end of February. Australian toll road operator Transurban has also reported an impact from the energy market shock on its traffic numbers for March and April 2026. This is out of step with history, where toll road traffic has historically been resilient in the face of higher petrol prices. This time, the speed and size of the increase seem to have driven a “sticker shock” that has hurt activity. Drivers have worked to conserve petrol and reduce trips in response to an initial jump in prices.

After an initial decline, we would not anticipate another leg down in activity from here. While softer activity can persist, conditions should not significantly worsen. Government actions to support hard-hit households and business sectors provide a cushion. This includes such measures as a temporary cut to the fuel excise in Australia, which is seen in the drop in the retail price from April 2026, and direct relief to end-users in France. There is also an argument for households adapting to the “new normal”, once initial fears of outright fuel shortages dissipate. Long-term, we expect structural growth in demand to support traffic volumes on well-positioned toll roads, with the current gas price shock a sharp, but transient, event.

By The Magellan Infrastructure Team

Important Information: Units in the fund referred to herein are issued by Magellan Asset Management Limited ABN 31 120 593 946, AFS Licence No. 304 301 trading as Magellan Investment Partners (‘Magellan’). This material is issued by Magellan and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to the relevant Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellaninvestmentpartners.com.

Past performance is not necessarily indicative of future results and no person guarantees the future performance of the fund, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. This material may contain ‘forward-looking statements’. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third-party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan.

Further information regarding any benchmark referred to herein can be found at www.magellaninvestmentpartners.com/funds/benchmark-information/. (080825-#W14)

By clicking “I Agree” you represent that you are a ‘wholesale client’ under section 761G of the Corporations Act 2001 (Cth) (the “Act”). Further, you represent that you will not directly or indirectly disseminate information contained on this website to a ‘retail client’ within the meaning of section 761G of the Act.

This website contains general information only and does not take into account any person’s investment objectives, financial situation or needs. Nothing contained in the website constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or other financial instruments.

Important Legal Information: The information contained in the Institutional section of this website is not intended to constitute:

any offer for sale or subscription of securities to the public in New Zealand in terms of the Securities Act 1978 of New Zealand (the 1978 Act) (or any statutory modification or re-enactment of, or statutory substitution for, the 1978 Act). Accordingly, no prospectus or investment statement for the purposes of the 1978 Act has been produced in respect of the information contained in the website and the information does not contain all the information typically included in a registered prospectus or an investment statement under the 1978 Act; or

the provision of "financial advice" under the Financial Advisers Act 2008 (the 2008 Act) (or any statutory modification or re-enactment of, or statutory substitution for, the 1978 Act).

By clicking "I agree," you agree that you have read the terms detailed below and confirm that:

1) you:

(i) are an "habitual investor" for the purposes of section 3(2)(a)(ii) of the 1978 Act. "Habitual investors" are persons whose principal business is the investment of money or who, in the course of and for the purposes of their business, habitually invest money; or

(ii) otherwise fall within one of the other categories set out in section 3(2)(a) of the 1978 Act, meaning that you are not a member of the public for the purposes of the 1978 Act; or

(iii) you are acting for a person described in (i) or (ii); and

2) you are a "wholesale client" for the purposes of the 2008 Act.

The information contained in the Institutional section of this website is intended only for institutions that are both (i) habitual investors or otherwise fall within one of the other categories set out in section 3(2)(a) of the 1978 Act and (ii) "wholesale clients" under the 2008 Act. Such persons shall be referred to as "institutional investors" herein. Persons who are not institutional investors should not review the information contained in the website. This website is supplied on the condition that it is not passed on to any person who is not an institutional investor.

Nothing on this website constitutes investment, legal, business, tax or any other type of advice. The information on this website does not take into account the particular financial and investment objectives, circumstances and needs of any person. Information on the website is not intended for investors in any jurisdiction in which distribution or purchase is not authorized.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.You are solely responsible for evaluating the risks and merits regarding the use of the website and any services provided within. Nothing contained in that website constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or other financial instruments.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an Institutional Investor and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for institutional investors in any jurisdiction in which distribution or purchase is not authorised.

The information is intended for institutional investors and consultants to institutional investors and is published for informational purposes only. The information is directed at informing persons falling within one or more of the following categories:

1) A government, local authority, or public authority;

2) A bank or insurance company;

3) A pension fund or charity;

4) An individual who is a "qualified client" under the Investment Advisers Act of 1940 and has experience in investment, financial and business matters to evaluate the risks of investing in securities;

5) Persons whose ordinary activities involve or are reasonably expect to involve them, as principal or as agent, in acquiring, holding, managing or disposing of investments for the purpose of a business carried on by them;

6) Persons whose ordinary business involves the giving of advice, which may lead to another person acquiring or disposing of an investment or refraining from so doing.

Persons who do not fall into one of the above categories should not review the information contained in this site.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an investment professional as that term is defined in the Handbook of the Financial Conduct Authority ("FCA") or that I am acting for an investment professional.

Information contained on the Institutional section of this website is not intended for investors in any jurisdiction in which distribution of the information or purchase is not authorized or permitted.

The information is exclusively intended for, and directed at, investment professionals and advisers to investment professionals. Any products and investment services that are referenced on this website are only available to, or will only be engaged in with, investment professionals. Investment professionals will usually fall within one or more of the following categories (terms used have the same meaning as in the FCA handbook):

1) An authorised person;

2) An exempt person;

3) A government, local authority (constituted in any jurisdiction) or an international organisation;

4) Any person whose ordinary activities involve him in carrying on an investment activity;

5) A person who is acting in their capacity as a director, officer or employee of the above.

Persons who do not fall into one of the above categories, or who do not otherwise constitute investment professionals, should not read or rely on the information contained on this website.

The information provided on this website is for information purposes only and nothing on this website constitutes investment, legal, business, tax or any other type of advice.

Any performance data shown represents past performance. Past Performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the risks associated with investments generally and the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

Magellan Investment Partners (UK) Limited (FRN: 1037936) is an appointed representative of Sentinel Regulatory Services Ltd (FRN: 1007093) which is authorised and regulated by the Financial Conduct Authority.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an "Accredited Investor" and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for accredited investors in any jurisdiction in which distribution or purchase is not authorized.

The information is intended for accredited investors and consultants to accredited investors, and is published for informational purposes only.

The term "Accredited Investor" is a defined term under the Canadian Securities Regulation and includes Institutional Investors, such as banks, insurance companies, trust and loan companies, and pension plans. It also includes individuals provided they meet certain net worth or income thresholds. For more information, refer to National Instrument 45-106 of the Canadian Securities Administrators or consult your legal adviser.

Persons who do not fall into the definition above should not review the information contained in the site.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an "Institutional Investor" and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for institutional investors in any jurisdiction in which distribution or purchase is not authorized.

The information is exclusively intended for, and directed at eligible counterparties or professional clients as defined under the German Securities Trading Act. For more information, consult your legal adviser.

Nothing on this website constitutes investment, legal, business, tax or any other type of advice. The information on this website does not take into account the particular financial and investment objectives, circumstances and needs of any person. Information on the website is not intended for investors in any jurisdiction in which distribution or purchase is not authorized.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

You are solely responsible for evaluating the risks and merits regarding the use of the website and any services provided within. Nothing contained in that website constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or other financial instruments.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an "Institutional Investor" and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for institutional investors in any jurisdiction in which distribution or purchase is not authorized.

The information is intended for institutional investors and consultants to institutional investors, and is published for informational purposes only. The information is directed at non-retail clients falling within one or more of the following categories:

1) A government, local authority or public authority;

2) A bank or insurance company;

3) A pension fund or charity;

4) An individual who provides one or more investment services on a professional basis;

5) Persons whose ordinary activities involve or are reasonably expect to involve them, as principal or as agent, in acquiring, holding, managing or disposing of investments for the purposes of a business carried on by them;

6) Persons whose ordinary business involves the giving of advice, which may lead to another person acquiring or disposing of an investment or refraining from so doing.

Persons who do not fall into one of the above categories should not review the information contained in the site.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an "Institutional Investor" and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for institutional investors in any jurisdiction in which distribution or purchase is not authorized.

The information is exclusively intended for, and directed at institutional investors, accredited investors and expert investors as defined under the Securities and Futures Act (Singapore) (“SFA”) For more information, refer to the SFA or consult your legal adviser.

Nothing on this website constitutes investment, legal, business, tax or any other type of advice. The information on this website does not take into account the particular financial and investment objectives, circumstances and needs of any person. Information on the website is not intended for investors in any jurisdiction in which distribution or purchase is not authorized.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

You are solely responsible for evaluating the risks and merits regarding the use of the website and any services provided within. Nothing contained in that website constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or other financial instruments.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am a "professional investor" as defined under the Securities and Futures Ordinance of Hong Kong (the “Ordinance”) and any rules made under the Ordinance, and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for institutional investors in any jurisdiction in which distribution or purchase is not authorized.

The information is exclusively intended for, and directed at, professional investors as defined under the Ordinance and any rules made under the Ordinance or as otherwise may be permitted by the Ordinance. For more information, refer to the Securities and Futures Commission of Hong Kong or consult your legal adviser.

Nothing on this website constitutes investment, legal, business, tax or any other type of advice. The information on this website does not take into account the particular financial and investment objectives, circumstances and needs of any person. Information on the website is not intended for investors in any jurisdiction in which distribution or purchase is not authorized.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

You are solely responsible for evaluating the risks and merits regarding the use of the website and any services provided within. Nothing contained in that website constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or other financial instruments.

Thank you for your interest. We are committed to expanding our institutional website to meet the needs of our global investor base. We do not, however, have content approved for your location at this time. For additional information please email institutional@magellanfinancialgroup.com.

Important Information

This document does not constitute an offer of units in a Magellan Fund in any jurisdiction other than Australia or New Zealand (or in jurisdictions where it is lawful to make such an offer). Applications for units in a Magellan Fund from residents outside of Australia and New Zealand may not be accepted.

By clicking on the "I Confirm" button below you are confirming that you are a resident of Australia or New Zealand (or that you are acting on behalf of a person who is a resident in one of those jurisdictions).