Stock Story: Evergy

With AI a key narrative in markets, the common conception is that infrastructure stocks sit outside of this major growth driver. However, this is not the case. One example is Evergy (EVRG), which offers a regulated channel to capture the US electricity demand upcycle across Kansas and Missouri. The company has exposure to growing power demand across the US, as data centres come online. The investment case has strengthened as demand has moved from pipeline opportunities to signed electricity service agreements (ESAs), supported by large-load tariff protections that reduce the risk of existing customers subsidising new data-centre infrastructure. Together with traditional replacement investment, this makes Evergy’s growth opportunity look increasingly transformative rather than merely incremental.

Company snapshot

Evergy is a US regulated electricity utility headquartered in Kansas City, Missouri, with generation, transmission and distribution assets. The company was formed in 2018 through the merger of Great Plains Energy and Westar Energy. Evergy operates primarily through Evergy Kansas Central, Evergy Metro and Evergy Missouri West, serving approximately 1.7 million customers across Kansas and Missouri.

The company’s growth outlook has improved materially, driven by large-load demand and grid investment. Importantly, the management team has a track record of disciplined capital allocation, consistent earnings delivery and constructive regulatory engagement, positioning Evergy well to execute through this once-in-a-decade capex cycle.

Demand surge: from pipeline to signed load

Evergy has become one of the clearer mid-cap regulated utility beneficiaries of the US data-centre demand cycle. The opportunity is increasingly supported by signed large-load ESAs rather than only customer enquiries.

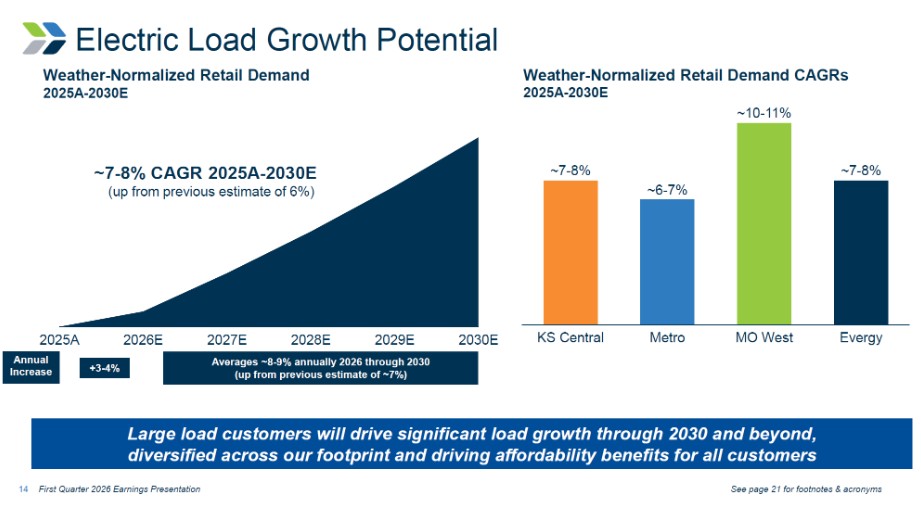

The demand outlook has been upgraded rapidly over the past 12 months. In 3Q25, Evergy was still framing demand growth mainly as upside: its base forecast was 2–3% demand growth until 2029, with potential to lift total retail sales growth to 4–5% if finalising agreements converted.

By 4Q25, the opportunity had started to crystallise. Evergy announced four large-customer ESAs, shifting the story from pipeline to contracted load. Management lifted its long-term demand outlook to ~6% weather-normalised retail demand CAGR for 2025A–2030E, with expected large-customer peak demand of ~2.4 GW.

The story improved again in 1Q26. Evergy signed a fifth ESA with a premier developer and amended two of the original four ESAs, adding incremental contracted load. Management raised its 2025A–2030E weather-normalised retail demand CAGR forecast to ~7–8%, while expected peak large- load demand increased to ~3.0 GW. Beyond the signed ESAs, expansion opportunities and projects in advanced discussions could add a further ~2.5–4.5 GW, providing additional upside to the current demand forecast.

This is meaningful relative to Evergy’s current system peak demand of approximately 10.6 GW. A ~3.0 GW large-load opportunity is equivalent to roughly 28% of today’s system peak. Demand growth is also broad across the footprint.

Source: Evergy Earnings Presentation 2026

The investment implication is significant. Higher load requires new generation, transmission and distribution investment, supporting Evergy’s updated 2026E–2030E capital plan of $21.6 billion, up 24% from the prior five-year plan. The company expects this capex plan to support ~11.5% rate-base CAGR from 2025E to 2030E, with the customer pipeline and future ESAs potentially driving further investment beyond the current plan. Accordingly, management has upgraded its adjusted EPS (earnings per share) growth outlook to 6–8%+ through to 2030, with more than 8% annual growth expected from 2028, compared with the prior 5–7% target in recent years. For context, a 1 percentage point upgrade is meaningful in the US regulated utility sector.

Regulatory backdrop: improving in Kansas and Missouri

Importantly, the quality of this demand opportunity is strengthened by improving regulatory frameworks in Kansas and Missouri. Both Kansas and Missouri are introducing tools that support investment in new generation, grid upgrades and large-load growth, while still protecting customers from excessive bill pressure.

Kansas has become a more constructive jurisdiction. HB 2527 provides utilities with stronger cost-recovery tools and mechanisms to reduce regulatory lag, supporting the potential for higher earned returns over time. The Kansas Corporation Commission has already applied these tools by approving recovery treatment for Evergy’s planned gas plants and solar project.

Missouri has historically been a more mixed jurisdiction, but the regulatory backdrop is improving. SB 4, signed in 2025, introduced supportive tools including timely recovery for new gas generation, expanded infrastructure recovery mechanisms and large-load tariff requirements. Together, these changes should reduce regulatory lag and improve Evergy’s ability to earn its authorised returns over time.

The commissions in Kansas and Missouri are also supportive of economic development and have maintained constructive engagement with utilities. Both states have approved Evergy’s large-load tariff structures for customers above 75 MW, with long-term contracts, minimum-bill requirements, collateral and termination protections. These provisions improve the quality of the data-centre opportunity by requiring durable customer commitments and reducing stranded-cost and cross-subsidy risk for existing customers.

Overall, Evergy’s data-centre story has three attractive features: signed customer agreements, regulated tariff protections and a direct link to generation and grid investment. The key risk is execution. Evergy still needs to deliver the required capacity, obtain regulatory approvals and manage customer affordability. However, the progression from 3Q25 to 1Q26 shows a clear positive inflection: demand growth has become a core driver of Evergy’s multi-year growth plan.

Fiona Wu, CFA, Investment Analyst

Important Information: Units in the fund referred to herein are issued by Magellan Asset Management Limited ABN 31 120 593 946, AFS Licence No. 304 301 trading as Magellan Investment Partners (‘Magellan’). This material is issued by Magellan and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to the relevant Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellaninvestmentpartners.com.

Past performance is not necessarily indicative of future results and no person guarantees the future performance of the fund, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan or the third party responsible for making those statements (as relevant). Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. This material may contain ‘forward-looking statements’. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third-party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan.

Further information regarding any benchmark referred to herein can be found at www.magellaninvestmentpartners.com/funds/benchmark-information/. (080825-#W14)